Retail loans portfolio grew by 13.6% from Mar’21 to Mar’22 with INR 85.2 lakh crores as of Mar’22

CRIF High Mark, India's leading credit bureau released its flagship report titled, How India Lends FY 2022, on the overall lending data that highlights key insights into Retail, Microfinance, and Commercial lending in India. The report is an annual issue to show historical trends in lending. Through this report, CRIF aims to provide insights to lenders and policymakers that will enable the overall development of the credit ecosystem.

Mr. Sanjeet Dawar, Managing Director, CRIF High Mark, said, “FY22 was a year of growth and revival for the financial services sector. The second edition of the ‘How India lends’ report relays that the Retail lending sector contributed 48.9% to the total lending market in India as of Mar’22. A growth rate of 38.5% in originations by volume is a positive indicator of the growth trajectory that the economy is witnessing, with Personal Loans, Consumer Durable Loans, and Gold Loans witnessing high Y-o-Y growth. As of Mar’22 we are affirmative that the Indian economy is on a path of recovery with abundant opportunities for the lenders to tap.”

The report deep dives into the analysis of retail loan products across personal loans, consumer durable loans, two-wheeler loans, home loans, auto loans, business loans, and credit cards. Below is a quick snapshot of the major loan categories:

Top Retail Lending Products:

By portfolio outstanding, home loans constitute the largest share of 29.9%, while consumer durable loans constitute the least share of 0.4%. In terms of active loans, credit cards constitute the market with a share of 17.2%, while auto loans constitute least share of 2.9%. Personal Loans, Consumer Durable Loans and Gold Loans witnessed highest Y-o-Y growth (by value and volume), as of Mar’22.

Below are the key highlights across growth, lender profiles and average ticket size for the different loan segments:

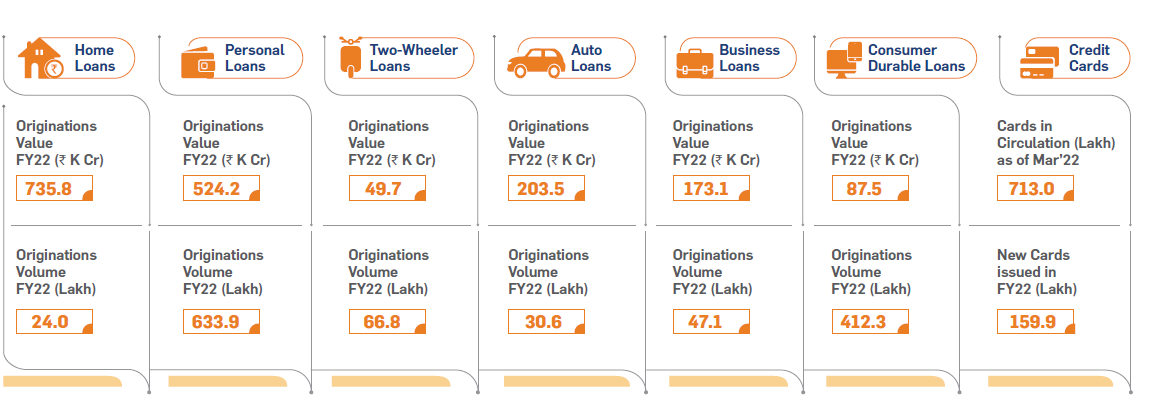

Home Loans:

The year-on-year growth in the overall portfolio was 13.3% on Mar’22 and 12.4% on Mar’21. Public Sector Banks and HFCs dominate the overall Home Loans by value and volume. The Portfolio outstanding (value) of Home Loans stood at INR 25.5 Lakh Cr as of Mar’22. The sector witnessed 29% growth in Originations (by value) and 20% growth in Originations (by volume) from FY21 to FY22. There is a 7.7% increase in Average Ticket Size for Home Loans from INR 28.4 Lakhs in FY21 to INR 30.6 Lakhs in FY22. The Average Ticket Size increased by 9% for HFCs, 8% for Public Sector Banks, and 6% for Private Banks from FY21 to FY22.

Personal Loans:

The year-on-year growth in the overall portfolio was 20.7% on Mar’21 and 22.4% on Mar’22. Public Sector Banks and Private Banks dominate Personal Loans by value with shares of 42.3% and 37.0% respectively.

NBFCs and Private Banks dominate Personal Loans by volume with a share of 47.4% and 31.2% respectively. Personal loans witnessed 46% growth in Originations by value, and 122% growth in Originations by volume from FY 21 to FY 22. There is a 33.6% reduction in Average Ticket Size of Personal Loans from INR 1.25 Lakhs in FY21 to INR 83K in FY22

Two-Wheeler Loans:

Two-wheeler loans had a portfolio outstanding of INR 77.9 K crores as of Mar’22. Two-wheeler loans witnessed 9.2% growth in Originations by value, and 2% growth in Originations by volume from FY21 to FY22, and the sector is dominated by NBFCs and private banks by volume and value.

Auto Loans:

Auto loans have a portfolio outstanding of INR 471.4 K cr as of Mar’22, with 8.3% Y-o-Y growth by value. Private Banks, Public Sector Banks, and NBFCs have a good presence in Auto Loans. There is a 23% growth in Originations (by value) from FY21 to FY22, an 8.6% growth in Originations (by volume) from FY21 to FY22. The average Ticket Size increased by 15.3% for Public Sector Banks, 12.8% for Private Banks, and 9.5% for NBFCs from FY21 to FY22.

Business Loans:

Business Loans include 5 account types namely Loans to Professionals, Business Loan General, Business Loan Unsecured, Business Loan Priority Sector Small Business, and Mudra Loans reported to CRIF High Mark Consumer Bureau. Business loans had a portfolio outstanding of INR 621.1 K crores as of Mar’22, with 12.2 % Y-o-Y growth by value and 11.1 % by volume. Public Sector Banks, Private Banks, and NBFCs dominate Business Loans (by value and volume) as of Mar’22. 10% growth in Originations (by value) from FY21 to FY22. 41% increase in Average Ticket Size from INR 2.6 Lakhs in FY21 to INR 3.7 Lakhs in FY22. Average Ticket Size increased for Public Sector Banks and NBFC while declined for Private Banks from FY21 to FY22.

Consumer Durable Loans:

Consumer durable loans had a portfolio outstanding of INR 37.4 K crores as of Mar’22, with 30.4% Y-o-Y growth by value and 22.3% growth by volume. Consumer Durable Loans witnessed 66% growth in Originations (by value) and 43% growth in Originations (by volume) from FY21 to FY22. These are dominated by NBFCs by both value and volume. The Average Ticket size increased for both Private Banks and NBFCs from FY21 to FY22.

Credit Cards:

Credit cards had total balances of INR 181.2 K (thousand) crores and 713 Lakh cards in circulation as of Mar’22. 48% growth in new cards issued from FY21 to FY22.